Kansas City’s hot real estate market pricing out many first-time, low-income buyers

READ MORE

‘Priced out’

Skyrocketing home prices across Kansas City have been good for sellers, but not necessarily for buyers. And none are having a harder time than low-income and first-time buyers.

Expand All

Kelly Allen barely snagged her Pendleton Heights house last spring.

She had been planning to buy a home for some time. And when the listing hit just a few blocks from her longtime rental home in historic Northeast Kansas City, she thought it might be her only chance to secure a house in the neighborhood she loved.

She didn’t bid more than other buyers. But she called the listing agent and offered to work with whatever lender they preferred. Likewise, she didn’t bring her own broker into the mix so that the listing agent could get both sides of the commission.

Allen also wrote the seller a “sad single mom letter,” telling him of her connection to the neighborhood as she pleaded with him to take her offer.

“By the skin of my teeth, I got this house,” she said. “I don’t know how people do it if they were even slightly less resourced than me. It’s incredible.”

But winning the bidding war wasn’t exactly the prize she envisioned.

To fit into her budget, she had to buy an older home that required work. Lots of it.

She paid about $130,000 — less than half the average home price of $268,158 in Jackson County, according to the Kansas City Regional Association of Realtors.

But since closing in April, she’s sunk $20,000 — nearly all her savings — into projects. And there’s still much more to do. The front porch is incomplete. Her bedroom floor is bare plywood. And she said the home desperately needs insulation before winter.

Though she frequently heard stories about buyers saving money compared to renting, she has seen her monthly housing payment change by only $1, from a previous rent payment of $810 to a monthly mortgage payment of $809.

“We’re going to live inside a project for a really long time,” she said. “I’m really grateful. I love the house, but I don’t know if this was a good decision.”

Home prices are skyrocketing in most parts of the country, including Kansas City, where supply has not been able to keep up with soaring demand. That was true before the pandemic, but the virus has only accelerated those trends.

Prices have made it difficult for nearly all buyers. But those buying for the first time have it especially tough since they have not benefited from rapid price appreciation the way existing homeowners have. And first-time house hunters have less buying power than ever. Though record-low interest rates have lured many to the market, they haven’t made up for the exponential growth in housing costs, which have far outpaced wage growth.

The current market has also squeezed out many working-class buyers.

That’s because home prices are rising the most on the most affordable properties, putting even more pressure on buyers at the lower end of the market.

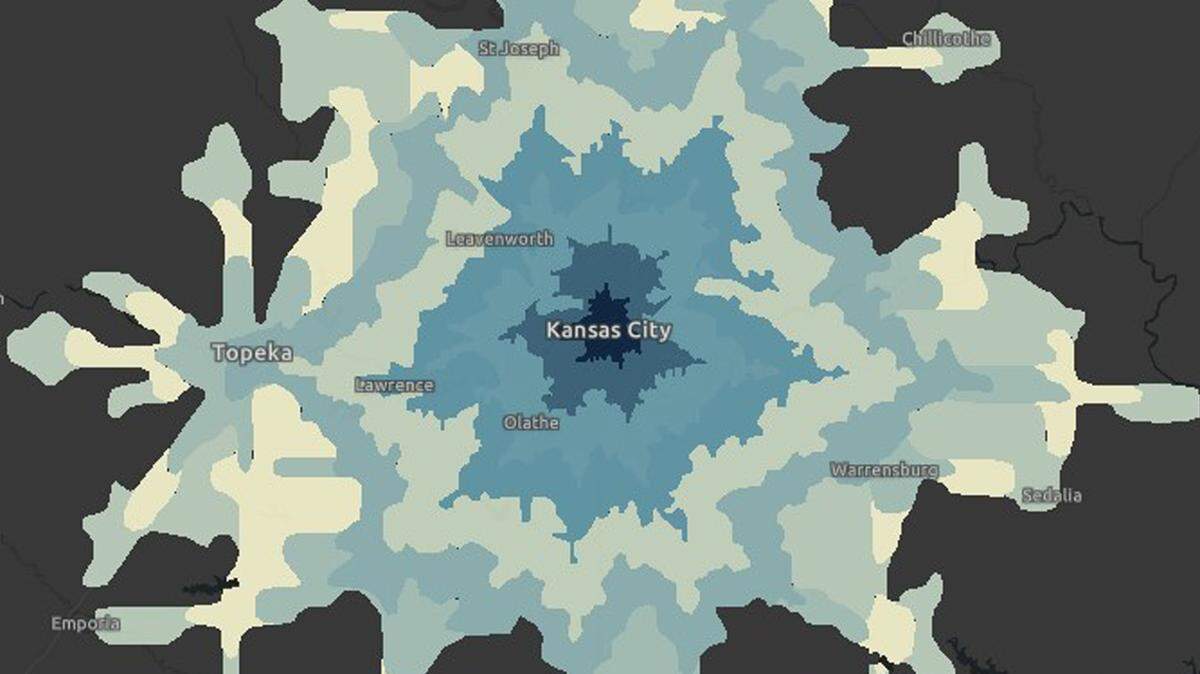

Kansas City’s housing market isn’t unique among American cities. But homes here move even faster than in other parts of the country, staying on the market for an average of three days, according to Zillow, an online real estate marketplace company.

In a sellers’ market, the most desirable properties frequently command multiple offers. And more than half of all homes are selling above list price, according to Zillow.

That environment has made it increasingly difficult for buyers in targeted homebuyer programs, like those who qualify for loans backed by the U.S. Federal Housing Administration and the U.S. Department of Veterans Affairs.

Those programs were designed to give certain buyers a leg up in the marketplace. But with additional inspection requirements and regulations, brokers say those offers are proving to be the least competitive nowadays. Some listings now explicitly state that the seller will accept only cash or conventional offers.

The National Association of Realtors says conventional mortgages accounted for about three-quarters of all mortgages obtained by buyers this May. That was a sizable increase from about 65% between 2018 and 2019. This year, the share of FHA-insured mortgages fell to 14% in May from about 20% in previous years. The share ofhttps://www.sacbee.com/money/best-va-loans/https://www.sacbee.com/money/best-va-loans/

also decreased to 7% in May 2021 from about 10% in past years.

Over that time period, local programs designed to help first-time and low-income borrowers have disappeared, said Turner Pettway, president and CEO at Neighborhood Housing Services of Kansas City Inc.

His organization previously offered counseling for first-time buyers with lower incomes but has largely stopped doing that. He said low- and moderate-income people increasingly don’t believe they can own their own homes.

“You’ve got so many folks that just cannot afford to save,” he said. “So I don’t think the average low- or moderate-income person is thinking about buying a house. That’s just not on the list.”

While appreciation has been good for many owners, housing advocates universally agree that what’s happening at the other end of the market is bad news for society. Homeownership is the greatest tool for building personal wealth — wealth that often lasts for generations in a family. And many people believe homeowners build more stable neighborhoods than renters do.

City programs used to provide down payment assistance and favorable loan terms that helped low-income buyers realize the dream of homeownership. But with many of those programs now defunct, those buyers are more discouraged than ever by steep prices.

“You don’t find that price point at $125,000 for a decent house with three bedrooms, a basement and a backyard. It’s very difficult now,” Pettway said. “In a way, people are being priced out of the market. This is where the government should come in, but it’s just not on the agenda.”

First-time challenges

Allen is the special projects director for Kansas City’s Lykins Neighborhood. And she’s been active in KC Tenants, which advocates for affordable housing and renters’ rights.

“Helping people figure out how to live affordably is what I do,” she said. “And it was still really freaking hard.”

Allen said the commodification of housing — intertwining housing with financial markets, rather than viewing a home as a basic need — has made it too expensive for someone to rent or buy in Kansas City.

That’s especially true in places like Pendleton Heights, which sits northeast of Independence Avenue and Interstate 29. It has seen a huge revival as investors and owner occupants have purchased and improved large historic houses. With new apartments and coffee shops nearby, homes there can now command well above $300,000.

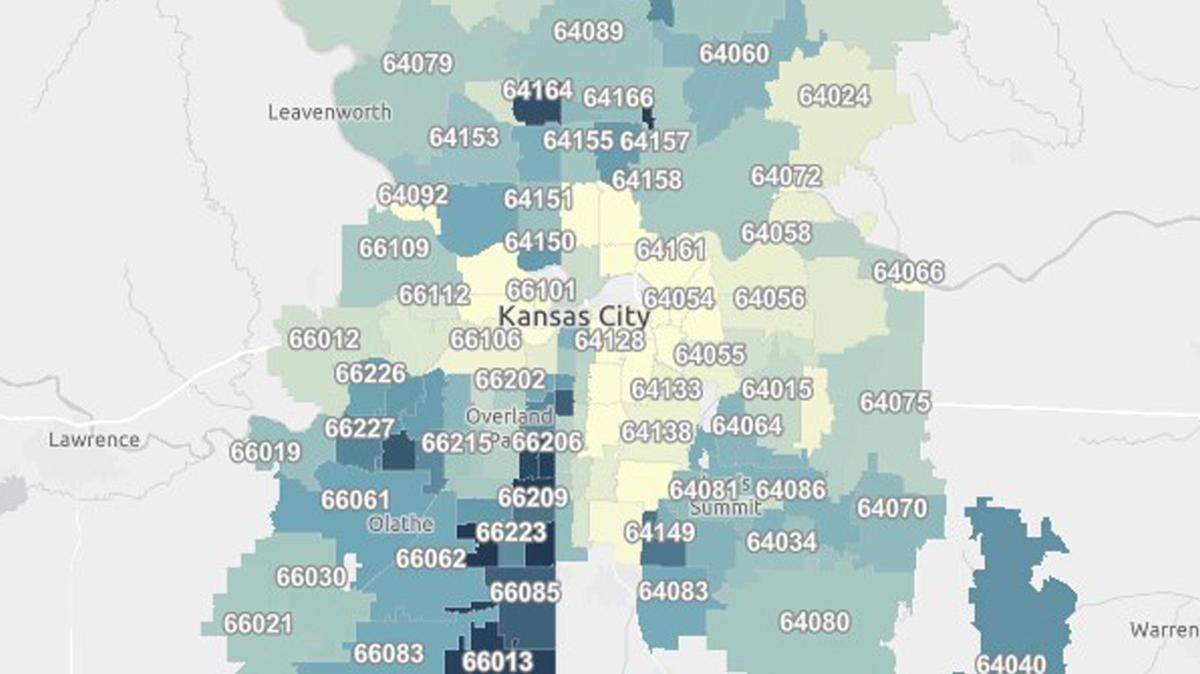

The area’s 64124 ZIP code has seen home values more than double over the past five years alone, according to Zillow.

“It’s not like the quality of life has doubled. It’s not two times as good here,” Allen said. “We still deal with all the things an inner-city neighborhood deals with. We just have to pay twice as much to do it.”

Allen said her income was low enough that she knew she would have qualified for an FHA loan.

But she also knew that such a financing package could make her offer a long shot. So she qualified for a conventional mortgage.

That’s probably wise in a market increasingly tilted against FHA buyers.

“There is loan discrimination that occurs in the market,” said Leslie Lowry, a senior mortgage adviser at Fairway Independent Mortgage Corporation. “I try to pre-approve (buyers) conventional at all cost.”

Lowry said sellers and their agents just don’t want to deal with the additional complexities of VA or FHA loans, particularly when they have other offers. Those government programs have certain standards about a home’s condition, meaning a seller might need to fix problems for the sale to go through.

That wasn’t such a problem a few years ago, when buyers could ask for all manner of repairs after home inspections. But now, many homes are selling as-is, and some buyers are waiving home inspections altogether to make their offers more competitive.

“They don’t want to mess with it,” Lowry said. “It always comes down to money, and that’s what this is about.”

Though the use of those programs has dropped, experts say some of that slack has been picked up by lenders with special programs of their own that mirror the benefits but allow buyers to still make offers with conventional mortgage products.

Commerce Bank, for instance, has helped 200 buyers get into homes through its Neighborhood Connection program, which targets low- and moderate-income neighborhoods.

Lowry said house hunting has been “brutal” for all first-time buyers, who face an entirely different market than buyers even a few years ago.

“Five or 10 years ago, there weren’t five or 10 offers on every single home,” she said. “And the days are long gone where you could buy a $100,000 home.”

While house prices have climbed dramatically, low interest rates have given today’s borrowers some relief. Research from the Federal Reserve Bank of St. Louis shows that the amount of disposable income Americans spend on mortgage payments in the aggregate has actually been declining as interest rates hover near 3%.

“That’s some of what is driving higher prices,” said Stanley Longhofer, a professor and director of Wichita State University’s Center for Real Estate. “People can buy so much more given their level of income.”

He said the market didn’t get this tight overnight: It was tightening for years as new home construction lagged after the Great Recession. But markets tend to find equilibrium, and Longhofer expects the real estate market to stabilize soon. Even if prices don’t drop, inventories should pick up and price appreciation will likely slow, he said.

“This had been building for seven or eight years,” he said. “We have to expect that it’s going to take a long period of time to work that back out.”

He’s not too fazed by the drop in FHA loans, which allow lower down payments for borrowers with less or worse credit than those who get approved for conventional loans.

“If an FHA loan is the only way you can get approved and you can’t get approved without having FHA, then you want to seriously ask yourself whether you’re actually ready for all the responsibilities of homeownership,” he said. “Which is worse: for somebody to not get into a home or for somebody to get into a home and then not be able to take care of it, not be able to maintain it, not be able to stay there and then end up losing the home?”

Millennials enter the market

Like marriage and child bearing, millennials put off home buying much longer than previous generations did.

While first-time buyers previously were making home purchases in their 20s, the typical first-time buyer’s age is now 34.

While they may have had longer to save, millennials are disproportionately burdened with huge amounts of student debt. And many stayed in school longer than previous generations, meaning they entered the workforce later.

The housing market millennials inherited was severely strained as new home construction plummeted in the wake of the Great Recession. Economists believe that new homes, even at higher price points, would help free up inventory of less expensive existing homes.

“We are at the tail end of a decade of severe underconstruction,” said George Ratiu, senior economist at Realtor.com. “There’s a massive shortage of new home construction.”

So when millennials finally went to the home market, they faced multiple headwinds unseen by previous generations.

“It’s unequivocally harder for many first-time buyers to actually get a foot in the door,” Ratiu said. “The fundamentals of the market — basically supply and demand — are out of balance.”

And while the coronavirus pandemic injected uncertainty into many parts of the economy, it only fueled the housing market, as people had more time than ever to consider what sort of home best suited their lifestyle.

“What the pandemic did was really accelerate a lot of people’s plans to buy,” Ratiu said. “Not only did people speed up some of their plans, first-time buyers tell us they were deciding to buy a home because of the pandemic.”

Millennials now account for the largest share of the American housing market. And experts don’t see that changing anytime soon: In a June survey by Zillow, about 3 in 5 millennials and Gen Z’ers said they planned to use money they saved during the pandemic toward a down payment on a home.

While prices can deter many from entering the market, they can also have the opposite effect. If people believe costs will only continue to rise, they may feel more pressure to get in now while they can, said Nicole Bachaud, an economic data analyst with Zillow.

“The majority of millennials are just now coming into home buying years,” she said. “This is where it’s going to hit the fan whether or not there was this pandemic effect in the market. We were going to have people buying over the next few years regardless.”

For some people, home values have climbed so much that it’s begun to make renting look more palatable. Zillow expects mortgage costs to continue to climb, while rents are expected to stay somewhat steady.

Zillow analysts do expect the market to simmer somewhat in the coming months. But Bachaud said prices are at risk of leaving many Americans out of the housing market.

“If we leave inventory where it is now, that could be likely in the future,” she said. “We could see such short supply that it is not possible for people to afford to get into homeownership.”

First-time buyers get creative

This market hasn’t totally upended things in Kansas City, where long-attractive neighborhoods remain in demand. Johnson County is still highly desirable, and homes in Brookside still fetch high prices.

But some neighborhoods like Waldo are so hot that they have become out of reach for many first-time buyers.

Consider how much prices have changed there in the past two years. In June 2019, Zillow estimated the typical home value in the area’s 64116 ZIP code at $207,659. By June of this year, that value had topped $255,000 — an increase of nearly 25% in just 24 months.

That sort of price appreciation — or one even more intense — is happening all across the metro. Realtor Stacey Johnson-Cosby said that’s pushed many first-time buyers to reconsider the location and style of the homes they want.

“They may have to change what they’re looking for, to adapt to the marketplace, and it may mean looking in a neighborhood that is not your ideal neighborhood,” she said. “Or, if you want a four-bedroom, be willing to accept the three-bedroom.”

Buyers who can’t muster that sort of flexibility may do best by staying on the sidelines, she said.

“If you don’t have patience and fortitude, you may want to sit it out, which is unusual for a real estate agent to say because I am all about people owning homes,” Johnson-Cosby said. “But this market is a market that is not for the faint of heart.”

Realtor Jim Godwin said all buyers need some extra education in this market. Most homes are going for over the asking price, and many buyers are forgoing inspections — an almost unfathomable practice just a few years ago.

“These are very new things, even in our world, that need to be explained to people so that they have a full understanding of what they’re getting into when they enter the marketplace for the first time,” he said.

Godwin said prices have pushed many buyers to Independence, Raytown and Raymore, where homes are more affordable.

“People are getting priced out of certain areas,” he said. “Lee’s Summit is a good example. Six years ago, seven years ago, it was pretty easy to find a house in Lee’s Summit that was affordable. Now, it’s almost impossible, especially for a first-time buyer.”

Research from Zillow shows prices are rising the fastest in areas closest to downtown Kansas City, where homes are generally more affordable. This year, the median value of a home within a 10-minute drive of downtown was $143,300 — a nearly 57% increase since 2019. Homes within a half-hour’s drive of downtown were valued at $305,900 — an increase of about 22% over two years.

But brokers say the opposite is also true.

Outlying areas have become more popular as buyers look for any respite from the market. Lower prices, paired with the rise of remote work, has made areas farthest away from the city, like Excelsior Springs, De Soto and even Warrensburg, more attractive lately.

“Maybe they don’t need to be in downtown Kansas City now. Maybe they can be in Raytown or out in the outskirts,” said Tony Conant, president of the Kansas City Regional Association of Realtors.

Conant is a Realtor in Warrensburg, which is getting more popular even for people who work an hour’s drive away in Kansas City. But as prices escalate there, he sees buyers moving on to other places like Holden, Missouri, a town of 2,400. Some new construction homes are selling for close to $200,000, he said. That’s less than half the average price of $468,955 for new construction in the Kansas City region.

Conant thinks the market has begun to ease ever so slightly. It feels like there is a bit more inventory to go around and somewhat fewer bidding wars. But he said home price appreciation will be a long-term challenge for minority and low-income families.

“This is going to be a problem,” he said. “And it’s going to affect a certain demographic of folks. And those are really folks we would like to most see get a home.”

Success stories

Bachir Diallo has a good-paying job in IT. But he’s lived in the United States only since 2017, so his credit history is short by most lender standards.

That led the 38-year-old immigrant from Guinea to look for an FHA loan, which provides a boost to people with lower credit scores.

When he started looking around, Diallo was shocked by both the prices and the speed of the market. He initially thought he could spend up to $350,000 to buy a first home for his family of five. But given the market realities, his agent suggested he look at homes priced closer to $280,000 to provide enough room for inevitable bidding wars.

“Seriously, it’s a bad time to buy,” he said.

He lost out on several different properties in Johnson County and ended up changing lenders to finally land his Lenexa home in July. The FHA program allowed for a much lower down payment, but Diallo knows he’s paying for it through higher interest rates.

While his rent was about $1,600 a month, his mortgage is about $2,100. All of his bills have increased, too. Being a first-generation immigrant, he also feels obligated to send a portion of his income back to family in West Africa.

“Sometimes it’s scary. You ask yourself why you put yourself into this situation,” he said. “After putting all I have into this, it’s like starting from scratch financially.”

But he believes that is a short-term problem.

“Looking at the long term, I know I’ve made the right decision,” he said. “It’s building a foundation for my kids when they grow up. Whether it’s this house or I sell it and move to another house, it’s the American Dream.”

That’s the dream Errienne Floden is chasing now.

She’s worked for years to repair her credit, a lengthy process that has involved paying off old student loans and contesting credit reports because of identity theft. Working with a financial counselor at Community Services League, she’s seen her credit score go from the 500s to close to 800 now.

She’s a graduate of the Grooming Project, which trains single mothers living in poverty to become dog groomers, and now works with dogs in Kansas City’s Northland.

Floden, 38, lives with her fiance and three children in a two-bedroom apartment near 31st and Troost. Her teenage daughters share a room, and her toddler son stays with her and her fiance.

“I really want to be able to give my kids a good stable place to stay that’s decent sized,” she said. “I want them to have a yard to play in.”

She’s been saving for a hefty down payment. And she knows she’ll probably need more cash for repairs and upgrades. With plans to spend up to $240,000, she didn’t expect to find a home in move-in condition.

“I’ve been watching the housing market for, like, well over a year now. I’ve definitely seen the prices go from quite affordable to kind of crazy,” she said. “If it’s even remotely good, it’s pending that day or the next day. They’re just flying.”

This has been a long and tough journey, she said. And it will mean a great deal to her and her fiance to have a place of their own after a lifetime of struggles. They’re currently living in transitional housing.

But Floden was adamant that she wouldn’t let the market, or her emotions, get the best of her.

“I’m not overpaying for a house,” she said just before she started the search process. “I’m looking to buy a house that I can have equity in and not be upside-down.”

A few days later, she got preapproved for an FHA loan, met with a real estate agent and began looking at listings.

Her family quickly found an 1,800-square-foot home in Independence they loved. A recent completion from flippers, the home is mostly ready to move in, though Floden is eyeing some small upgrades.

They offered $225,000 for a home listed at $227,900. After some negotiation, both sides agreed on a sale price of $228,900 and the seller agreed to add a stainless steel stove to match the other kitchen appliances. With inspections coming soon, Floden expects to close in late September.

“It’s been a long road to get here,” she said, “and honestly, both of us never thought we would.”

This story was originally published September 1, 2021 at 5:00 AM.