If you walk into the CFP® exam expecting flashcards and formulas, you’ll be caught off guard.

This exam tests how you think, not just what you can memorize, making it harder than the average test. In fact, as of July 2025, only 64% passed. And it’s long: 170 multiple-choice questions split into two subsections, with one optional break. To pass, you must demonstrate not only technical knowledge, but also the ability to reason through real-world scenarios—all with some serious stamina.

In this guide, I’ll break down the exam content, show you how to approach scenario-based CFP® exam questions, and highlight key factors to focus on.

Key Takeaways

- Practice questions simulate reality: Scenario-based items require logic, not rote memorization.

- Investment & taxation concepts matter: Expect repeated questions on stock valuation concepts, investment risk, taxable income, retirement plans, and GST tax compliance.

- Client context is everything: You’ll interpret plan selection, beneficiary designations, planner attitudes, special circumstances, and investment vehicles.

- Real exam structure: 170 questions, two sections, short scenarios, stand-alone questions, and case studies.

- Financial planning mindset: Demonstrate ethical conduct, client protection, and practical guidance like a true Certified Financial Planner.

What the CFP® Exam Covers

The CFP® exam assesses your ability to implement the financial planning process, not just how well you can memorize definitions. Each domain uses scenario-based questions, short scenarios, and stand-alone questions to test your professional judgment.

Topic areas include:

- General principles of planning

- Investment planning

- Income taxation & tax planning

- Insurance planning and risk management

- Retirement savings & qualified plan rules

- Estate planning

- Financial planning for special needs & special circumstances

CFP® exam questions don’t ask: What is the definition of risk?

They ask: A 49-year-old business owner with a volatile income stream wants a steady retirement vehicle. What’s the most appropriate choice based on her risk tolerance, tax consequences, and business structure?

Why Application Is More Important Than Memorization

The CFP® exam forces you to translate quantitative investment, income taxation, and professional conduct concepts into decisions. You’ll see references to:

- Client’s risk tolerance vs. investment risk

- Investment vehicles vs. liquidity needs

- Bond and stock valuation concepts vs. retirement goals

- Insurance planning vs. family size

- Estate planning vs. beneficiary designations

Just like real life, there is rarely a single “perfect option.” You must choose the appropriate choice, not the mathematically ideal one.

Example:

A client wants a higher return than a savings account, fears stock market volatility, and needs funds in 18 months. CFP® questions will test whether you choose a short-term bond fund, CD ladder, or high-yield savings account, not whether you can write an essay on risk tolerance.

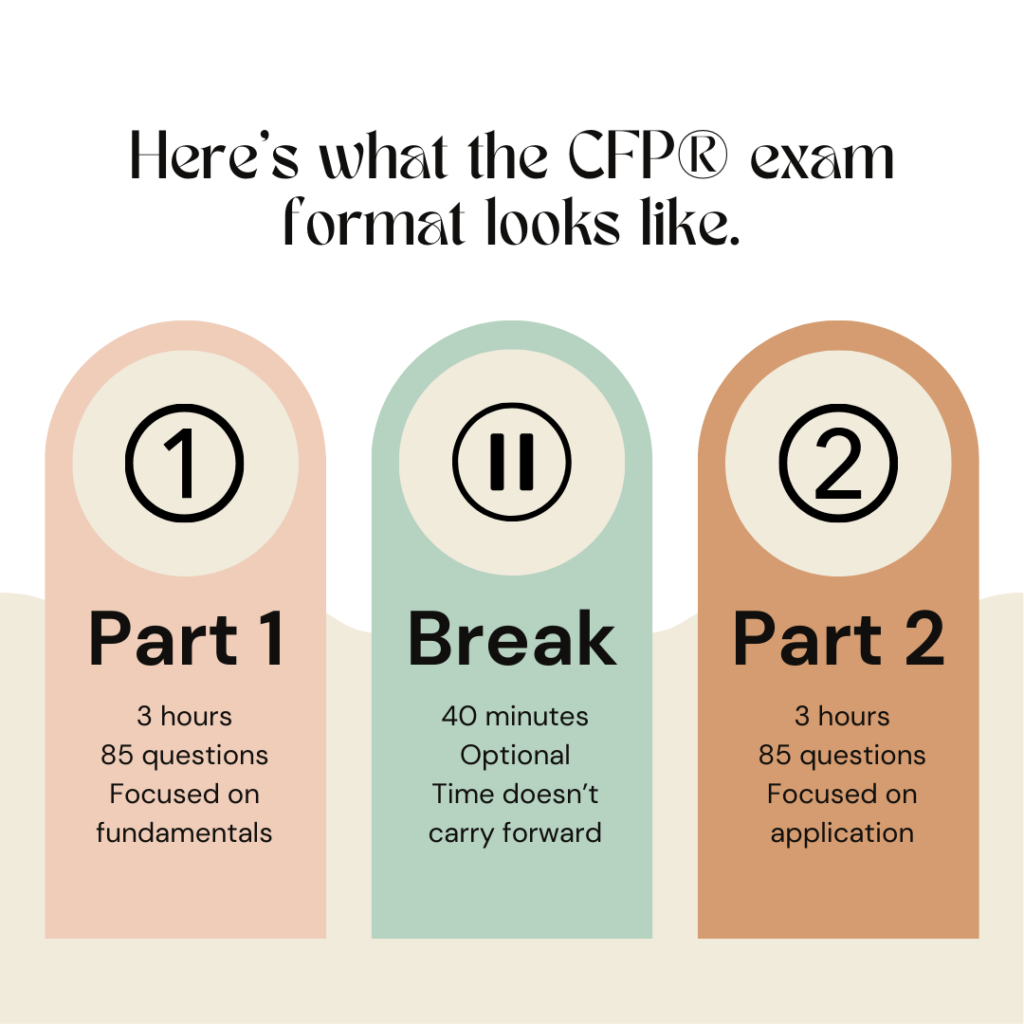

Exam Format: How the 170 Questions Work

The exam presents 170 questions across two main parts, each lasting three hours:

First Session

- About half of the questions

- Mix of standalone multiple-choice questions & short scenarios

- You do not see the second section until you submit

Optional Break

- 40 minutes

- Not mandatory

- Time does not carry forward

Second Session

- More complex scenario sets

- Multi-step case studies

- Heavy emphasis on retirement plans, tax planning, income planning, insurance, and estate topics

Remember: the passing score isn’t a published percentage. It is scaled, based on standards set by the CFP® Board. Study for mastery, not a number.

Study Strategy: Practice the Way the Exam Thinks

The best candidates don’t memorize PDFs or “money concepts” lists. They practice applying concepts to real exam logic.

Use realistic practice questions that mirror:

- Risk exposures

- Tax consequences

- Plan selection

- Investment strategies

- Insurance coverage

- Client priorities

- Special needs planning

Suggested Study Flow

- Start with sample questions in every domain

- Investment planning

- Retirement savings & qualified plan rules

- Estate planning

- Business entities & distribution rules

- Rotate topic areas weekly

- Avoid reading a single subject for 30 days straight.

- Simulate timing

- Practice under exam conditions with a timer

- Avoid calculator or internet crutches

- Find weaknesses early

- Identify where your “gut guessing” leads you astray

Sample CFP® Exam Questions (Exam-Style)

These items mirror the tone and logic of the real exam, not quick trivia.

1. Investment Risk

A 41-year-old teacher wants to increase retirement returns but fears volatility. Which investment vehicle is the most appropriate?

A. Leveraged equity fund

B. High-yield savings account

C. Short-term bond ladder

D. Cryptocurrency index

2. Tax Planning

A physician contributes to a non-qualified deferred compensation plan. Which statement is correct?

A. The employee is taxed when benefits are paid

B. All distributions are tax-free

C. The employer receives no tax benefits

D. Contributions automatically reduce AGI

3. Medicare Planning

A newly retired individual ages into Medicare. Which coverage handles outpatient services?

A. Part A

B. Part B

C. Part D

D. Medigap only

4. Business Entities

A sole proprietor wants to lower liability exposure and allow partner ownership. Which choice is best?

A. LLC

B. C-Corp

C. S-Corp

D. Schedule C

5. Retirement Plans

An unmarried couple with two children wants assets passed tax-efficiently. Which is best?

A. Joint TOD brokerage

B. Traditional IRA with spouse beneficiary

C. 401(k) with contingent beneficiaries

D. UTMA for children

6. Insurance Planning

A 32-year-old with two young children needs income replacement first, not investment growth. Which is most appropriate?

A. Term life insurance

B. Variable universal life

C. Whole life

D. Indexed universal life

7. Investment Strategies

A risk-averse client needs moderate growth and monthly liquidity. Which strategy aligns best?

A. 100% equity index fund

B. Laddered short-term bond funds

C. Cryptocurrency basket

D. Venture capital fund

8. Estate Planning

A client wants to transfer assets now while minimizing estate taxes and retaining no control. Which tool is most appropriate?

A. Payable-on-death account

B. Irrevocable trust

C. TOD deed

D. Revocable living trust

9. Income Planning

A 65-year-old retiree wants a guaranteed monthly income for life. Which product best fits this goal?

A. Immediate annuity

B. Corporate bond fund

C. REIT shares

D. Treasury STRIPs

10. Stock Valuation Concepts

A client wants to evaluate whether a stock is overpriced relative to earnings. Which metric is most relevant?

A. Price-to-earnings ratio

B. Sharpe ratio

C. Dividend payout ratio

D. Beta

Answer Key

- C: Short-term bond ladder

Conservative, stable, and suitable for someone who fears volatility but wants growth. - A: The employee is taxed when benefits are paid

Non-qualified deferred comp is taxable upon distribution, not contribution. - B: Medicare Part B

Part B covers outpatient medical services. - A: LLC

An LLC reduces liability risk and allows multiple owners. - C: 401(k) with contingent beneficiaries

Allows direct beneficiary designations and bypasses probate. - A: Term life insurance

Provides the highest death benefit per premium dollar for income replacement. - B: Laddered short-term bond funds

Moderate growth, lower volatility, and monthly liquidity. - B: Irrevocable trust

Removes assets from the estate and transfers control permanently. - A: Immediate annuity

Provides guaranteed income for life. - A: Price-to-earnings ratio

Directly evaluates market price relative to company earnings.

How CFP® Questions Are Designed to Trick You

Watch for:

- Client age vs. plan availability (Roth eligibility, catch-ups, RMDs)

- Pre-tax vs. after-tax contributions

- Life insurance vs. income replacement

- Long-term growth vs. immediate liquidity

- Risk tolerance vs. risk exposures

- Non-qualified plan rules vs. qualified plan rules

The wrong answer is often slightly logical but misaligned with:

- Time horizon

- Regulatory rules

- Client goals

- Professional conduct standards

- Consumer protection laws

Professional Conduct Matters More Than Math

The CFP® Board cares deeply about ethics. Expect scenario-based questions on:

- Dishonest communications

- Misleading return promises

- Conflicts of interest

- Beneficiary mishandling

- Duty to disclose compensation models

- Misaligned investment recommendations

Your planner attitudes are tested every bit as much as your calculations and education.

How to Register & Prepare

Exam registration is handled directly through the CFP® Board. You’ll select your testing window, submit application materials, and confirm eligibility before scheduling your exam date.

When choosing from the best CFP® prep courses, prioritize providers that simulate real CFP® exam questions, not just flashcards or short-term memorization tools.

Boston Institute of Finance

Known for structured, instructor-led CFP® programs and comprehensive review modules. Boston Institute of Finance CFP® curriculum mirrors real case study logic, helping you practice reasoning through tax planning, retirement scenarios, risk management, and estate decisions. Learn more in my review of Boston Institute of Finance CFP®.

Kaplan

Kaplan’s CFP® prep focuses on realistic timed exams, short scenario drills, and adaptive practice tests. Their question banks are designed to mimic real client conversations, income planning, insurance selection, investment vehicles, and special circumstances. See my full Kaplan CFP® course review.

Look for platforms that offer:

- Timed practice exams

- Case studies that span multiple domains

- Detailed answer explanations (why each choice is wrong or right)

- Coverage of core CFP® topic areas, including investments, income taxation, retirement plans, and client risk tolerance

You are not preparing to memorize a list of rules; you are preparing to think like a planner who guides real people with real consequences.

Final Thoughts

CFP® exam questions are designed to reflect the real craft of financial planners: balancing risk, income, retirement savings, insurance, estate, and business considerations while honoring the client’s well-being.

If you study only definitions or stock market trivia, you’ll struggle. Instead, focus on learning to reason through scenario-based questions, understand retirement, investment, and insurance plans, and apply tax concepts to real-world examples. Then, you will walk into the exam confident and prepared.

FAQs

A mix of stand-alone multiple-choice questions, short scenarios, and multi-step case studies.

Yes. It tests real client planning, not memorization, and requires strong reasoning.

170 questions are split into two sections, with an optional break in between.

Different hard, CPA is technical, while CFP® is application-based and client-focused.

The CFP® Board uses a scaled score; no fixed percentage is published.